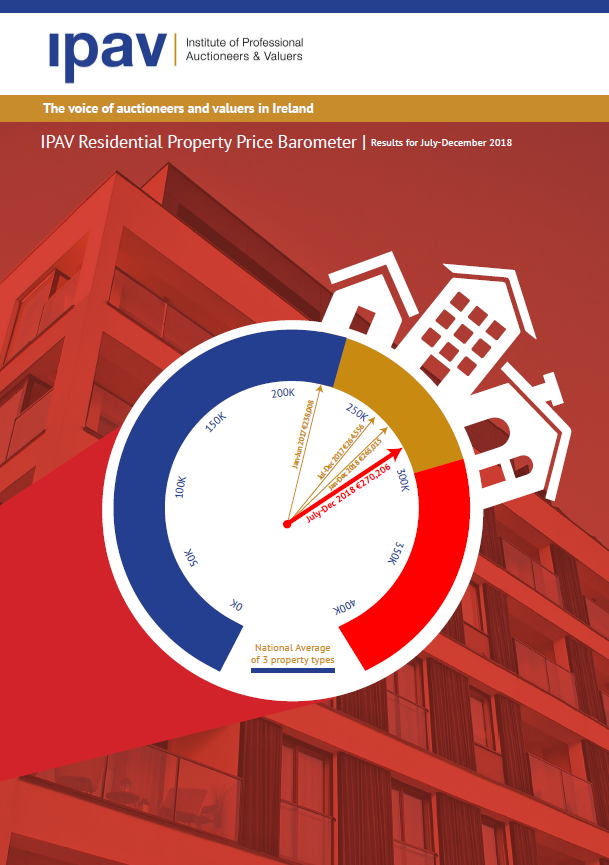

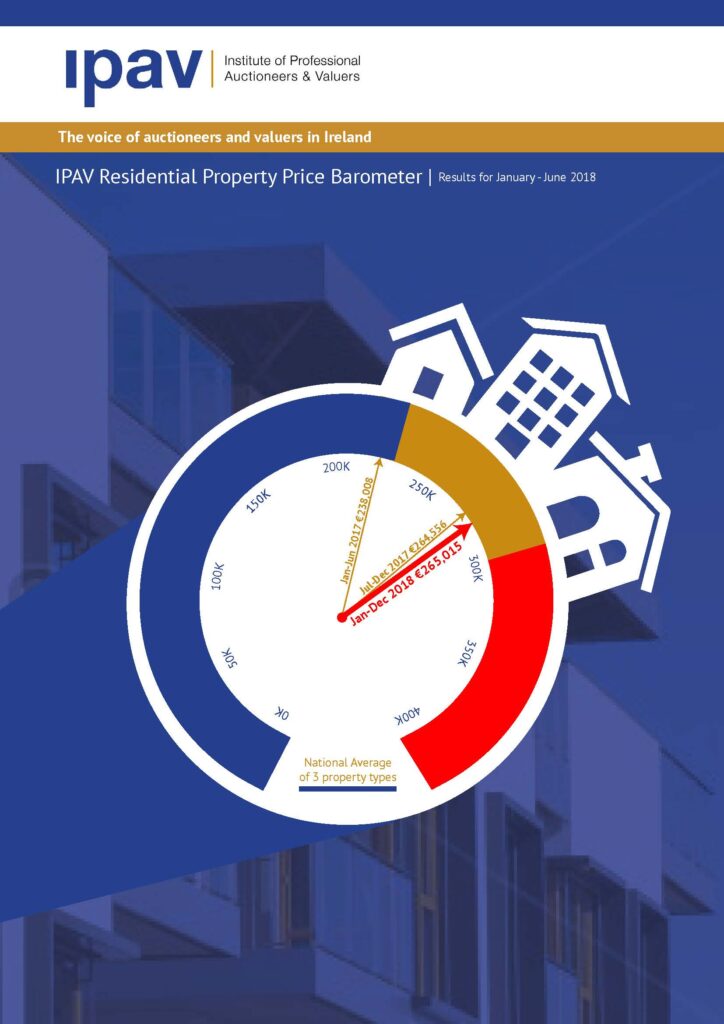

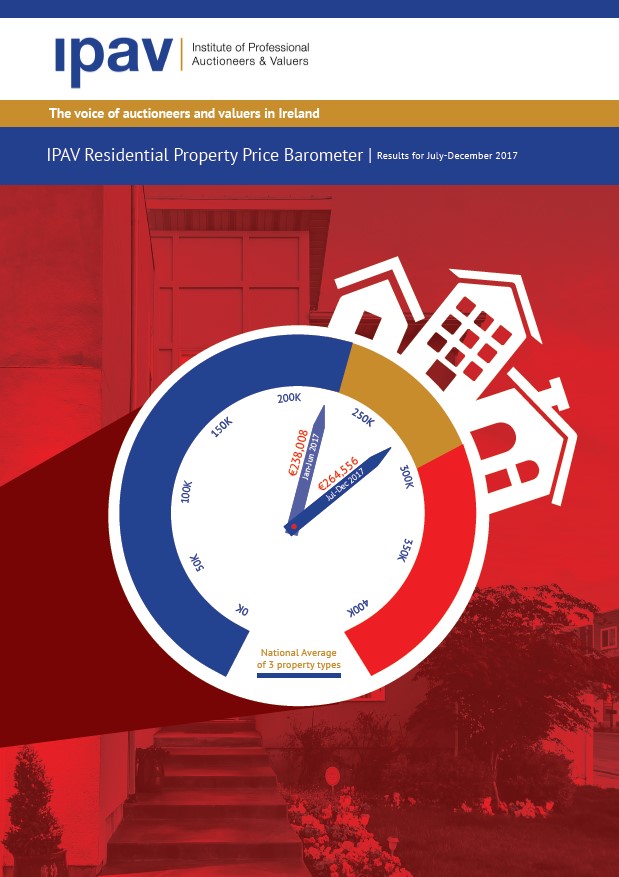

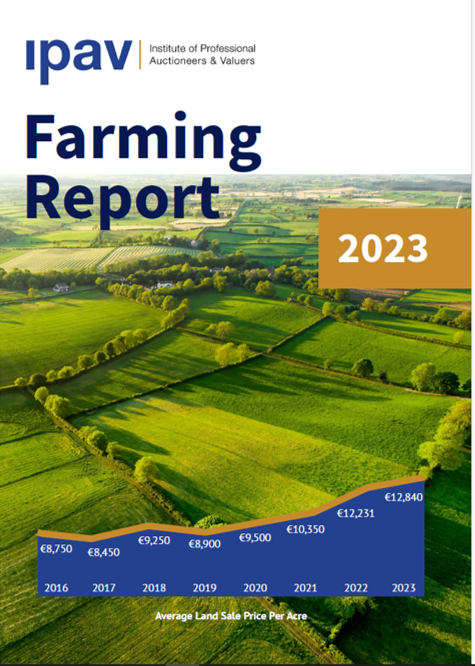

Submissions & Reports Here, you'll find IPAV’s insight and commentary on industry news and developments. IPAV Property Price Barometer 2025 Q1 & Q2 IPAV Farming Report 2024 IPAV Property Price Barometer 2024 Q3 & Q4 IPAV Property Price Barometer 2024 Q1 & Q2 IPAV Property Price Barometer 2023 Q3 & Q4 IPAV Property Price Barometer 2023 Q1 & Q2 IPAV Property Price Barometer 2022 Q3 & Q4 IPAV Property Price Barometer 2022 Q1 & Q2 IPAV Property Price Barometer 2021 Q1 & Q2 IPAV Property Price Barometer 2020 Q3 & Q4 IPAV Property Price Barometer 2020 Q1 & Q2 IPAV Property Price Barometer 2019 Q3 & Q4 IPAV Property Price Barometer 2019 Q1 & Q2 IPAV Property Price Barometer 2018 Q3 & Q4 IPAV Property Price Barometer 2018 Q1 & Q2 IPAV Property Price Barometer 2017 Q3 & Q4 IPAV Property Price Barometer 2017 Q1 & Q2 IPAV Farming Report 2023 & Press Release IPAV Farming Report January 2023 IPAV Virtual 2021 Farming Report Launch Upcoming Events Newsletters Magazines Press Releases IPAV in the news Interviews Submissions & Reports